By Josh Lehner,

Office of Economic Analysis,

Economic growth is surging as the pandemic wanes. Thanks to federal fiscal policy, consumers have higher incomes today than before COVID-19 hit. Now they are increasingly allowed to and feel comfortable resuming pandemic-restricted activities like going out to eat, on vacations, getting haircuts and the like. The outlook for near-term economic growth is the strongest in decades, if not generations.

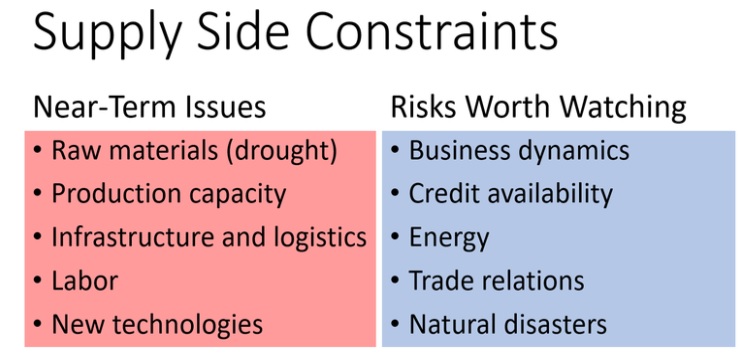

Given the strong underlying drivers of growth, the question becomes just how fast can the economy actually grow? Already supply constraints are evident in semiconductors, lumber, and rental cars to name a few. See our office’s table below for a broader view. Moving forward other short-term challenges of supply keeping pace with demand will emerge as well. Much of these constraints are expected to be temporary. Increased production and more efficient logistics will boost supply while higher prices and slower income growth as the federal aid runs out will cool demand somewhat. Better balance can be expected, although the path forward this year will likely be bumpier than expected.

The good news is some classic supply constraints like energy costs and credit availability are not currently issues holding back economic growth. The current issues largely revolve around production capacity, getting goods to market, and labor availability.

Currently, inventories are lean and demand is strong. Production needs to increase to meet the strong level of sales, which boosts overall economic growth. However many manufacturing sectors are already operating at or near capacity. They are constrained. To produce more, these industries need to invest in new plants and equipment, or add another shift. The overall economy reached this same point back in 2018-19 but the business investment never fully materialized as the trade war dampened demand even as the corporate tax cuts boosted incentives. This was before the pandemic put all investment plans on hold.

Today, these constrained sectors are currently facing the same choice, which has macroeconomic implications. On one hand, sales are high. To meet this demand and chase market share, profits, and the like, they need to make big, long-term investments. On the other hand, it is somewhat questionable just how sustainable these level of sales will be given the temporary federal boost to incomes, and the pandemic shifting consumer spending out of services and into durable goods and eating at home. See Jason Furman’s recent post and charts for a good look at current spending relative to trend.

Note that the constrained industries and those near capacity represent a 40% larger share of Oregon’s economy than they do nationwide (11.8% of Oregon GDP vs 8.3% of US GDP). We will have more on the regional manufacturing outlook in a follow-up post.

Overall, the best economic outcome would be to see new investments in production, which boosts both near-term growth, and raises long-run potential GDP as the productive capacity of the economy increases. The good news is that while industrial capacity as measured in real time in the Fed’s data isn’t really picking up yet, new orders for capital goods are booming, as is business investment in IT and software. Encouragingly R&D spending is doing well, and we might get additional federal spending in the pipeline too.

Now, of course the worst economic outcome here would be that production continues to be throttled due to capacity constraints and results in higher inflation but no real capacity increases.

Even so, the most talked about constraint on the economy today is labor, in part because it runs through all of these other issues. Attracting and retaining workers is already much more challenging than expected given the economy went through a severe recession last year. There are a variety of simultaneous factors impacting the number of available workers including strong household finances, the virus itself, and lack of childcare or in-person schooling. (See our office’s joint report with the Employment Department for more.) And while the temporary pandemic-related constraints will ease in the months ahead, the labor market is expected to remain tight for the foreseeable future in large part due to demographics and the large number of Baby Boomers retiring. Labor will remain a challenge for firms. But a tight labor market also works wonders for employees with strong wage gains and more plentiful job opportunities.

Outlook: This cycle is different. Overall the expectations are for exceptional economic growth this year and strong gains next. This economic recovery is front-loaded, unlike the last couple of long-lasting, demand-driven recessions. As such the risks primarily lie to the downside, not in terms of a double-dip recession, but in terms of growth “merely” being very good this year. That said, depending upon your horizon, these differences are not immaterial. Take our office’s forecast for example. The difference between a front-loaded recovery (red line) versus one that is not (dotted black line), has a big impact on the upcoming two year budget. The slower-paced recovery seen in the December forecast has average employment that is 2.7 percent lower over the next two years than the current, front-loaded outlook. Aggregate wages are 1.7 percent lower. (The smaller wage impact is due to the faster wage gains in recent months). Even as the current recovery will be stronger and more complete than recent cycles, the differences seen here are what you might expect in terms of growth in a supply-constrained economy.

Finally, for more on these issues, please see our latest economic and revenue forecast document. There is a good six pages on these supply constraints (with an Oregon focus) and another two pages on inflation. See our recent post on the drought, which is another supply constraint. Stay tuned for future posts on the local Oregon manufacturing outlook, and on the wage forecast.

Disclaimer: Articles featured on Oregon Report are the creation, responsibility and opinion of the authoring individual or organization which is featured at the top of every article.