But why? The easiest explanation to discard is that, in a race to the bottom, states have reduced corporate income-tax (SCIT) rates. They haven’t. Marginal SCIT rates have been more or less constant for more than 30 years.

Me? I attribute the decline in SCIT to increased tax avoidance/evasion. Tax avoidance/evasion isn’t a new enterprise, but its direction and focus changed dramatically after 1980 and it has been growing in size and sophistication ever since. The simple fact is that it is ridiculously easy for multi-state businesses to shelter profits from SCITs, reporting them where state corporate income-tax rates are low (in states like Nevada or Washington) and avoiding them in high-tax states (like Pennsylvania or Iowa). These days, this can be done with a couple of mouse clicks (and some accounting and legal legerdemain). Unfortunately, it’s hard to fix tax avoidance/evasion mechanisms or even say which ones matter most at the state level. Multi-state businesses are not required to publicly report the income taxes they pay in each state, just the total.

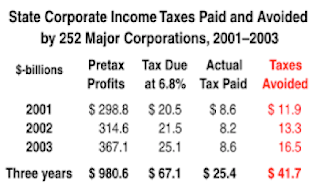

However, we know the nation’s output-weighted average state corporate tax rate is about 7 percent, while the average state corporate income-tax rate paid by profitable Fortune 500 C-corps is less than half that, which is a lot of avoidance, if not evasion.

Many of our colleagues deny that the massive decline in the weight of state SCIT revenue (which is itself unquestioned) is due to increased tax avoidance/evasion. They note that enactment of the pass-through provision in 1986 and its subsequent expansions have fundamentally transformed the business landscape in America, leading to a decline in C-corporations relative to pass-through businesses.

Under the U.S. tax code the profits (income) of publically held or C-corps are taxed twice, first through corporate income taxes and then again through personal income taxes on dividends and capital gains. Other businesses – individually, family, or employee owned – are all eligible for pass-through status, meaning that their income passes directly to their owners’ personal income tax returns, as are most partnerships (these businesses are not necessarily small; there are nearly 1,000 of them in Oregon with over 100 employees). As a result, the owners (shareholders) of C corps tend to pay higher tax rates on their businesses’ profits than do the owners of other businesses. That is generally also true at the state level. It is almost certainly the case in Oregon.

Consequently, pass-through businesses now account for more than 50 percent of all business income in the U.S., triple what it was in 1986. In fact, there are only about 3,500 large publicly traded companies in the U.S., down from more than 5,000 in the mid-80s. This goes a long way to explaining the relative decline in the importance of the federal corporate income tax vis á vis personal income tax receipts.

However, if that were the whole story, the decline in the relative importance of state corporate income-tax revenues would have been proportionate to the relative decline in the federal corporate income tax. Instead, it has fallen nearly twice as fast. Or, perhaps, more clearly, since 1990 total federal corporate tax revenues have grown about as fast as C-corp profits; total state corporate tax revenues have grown only half as fast. As a consequence, state corporate income-taxes now account for less than 2 percent of annual state revenues nationwide, down from 2.7 percent in the decade of the 1990s and 3.5 percent in the 1980s. In Oregon, the proportional decline has been less dramatic, from 1.8 percent of total state revenue, to 1.9 percent, and now 1.4 percent, according to Governing Magazine.

The decline in the relative contribution of Oregon’s CIT is proportionally less than in most states, especially places like Connecticut, Louisiana, Michigan or Ohio, where real corporate income revenues actually declined by more than 50 percent after 1990, but it still looks to be significant (although, in reality, probably not, since GM evidently excluded revenue from turnover taxes from its figure – see my next post).

Others of our colleagues are more conspiratorially minded. They tend to hold to an older view of corporate income taxes, which posits that the incidence of the tax is entirely shifted to other, less mobile, factors of production (labor and real property). Consequently, it follows that states should not tax corporate income, that, to avoid adverse effects on investment, output, and employment, it would be better to tax labor/land directly. While this view cannot be entirely ruled out as a theoretical matter, it’s wholly inconsistent with the best empirical evidence. For that reason, most tax economists now reject it.

Nevertheless, it might be noted, that, under this view, state elected officials choose to tax corporate income only because they are forced to by popular sentiment (“I pay taxes, but big companies get away Scot free?”). Bizarrely, some of those who hold this view assume a level of rationality on the part of state tax authorities that beggars all belief: they adopt high statutory tax rates to appease the public, but consciously mitigate their effects through special tax breaks. Hence, one observes persistent high state corporate income tax rates along with diminished collections.

However, as the Governing Magazine. article clearly shows, the scale of SCIT tax breaks is nowhere close to accounting for the relative decline in SCIT revenues. If nothing else, that should put paid to this particular conspiracy theory.

If I am right, tax avoidance/evasion is at the heart of the problem of the mystery of declining SCIT revenue, what can be done about it? I offer one answer in my next post.

Disclaimer: Articles featured on Oregon Report are the creation, responsibility and opinion of the authoring individual or organization which is featured at the top of every article.